The Gen Z Freelance Movement and the Tax and Bookkeeping Challenges That Come With It

More popular than ever

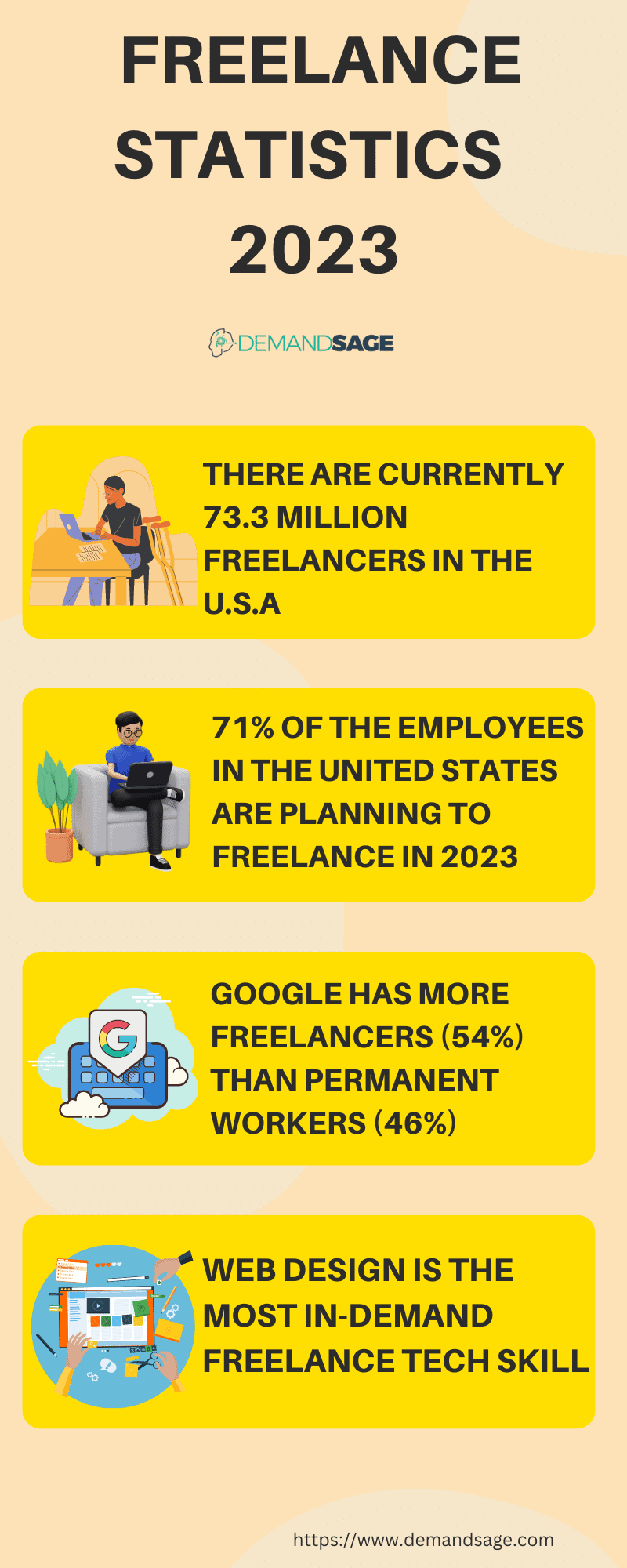

If it seems like more and more employees are turning to freelance work these days, you're not imagining things. According to one recent study, there are currently 73.3 million freelancers in the United States alone. The fast-paced mobile era that we're now living in, coupled with the advent of the fabled "Gig Economy" and companies like Uber and Lyft, have certainly helped bring this about. But what is fascinating isn't necessarily how many freelance workers there are - it's who, exactly, is doing the freelancing.

{kind=link}

Another study indicated that Generation Z in particular seems particularly fascinated by the idea of striking out on their own, with 53% of them having chosen self-employment of this nature in most cases. Approximately 50% of all Generation Z respondents to one survey, meaning those who fall between the ages of 18 and 22), engaged in freelance work of some kind.

It makes sense that people would want to have more control over their own employment and their ability to earn a living. That doesn't mean it is easier than "traditional employment," however - especially when it comes to the financial side of the equation. Bookkeeping and especially taxes present significant challenges that people need to understand before choosing to go down this path moving forward.

The Financial Side of Generation Z and Freelancing: An Overview

One of the biggest challenges that freelance workers of all generations have to deal with has to do with the idea of paying self-employment taxes.

Not only is it easy to suddenly find yourself working a freelance job - it can also happen very quickly. This is true to the point where someone may have made the decision without taking the time to research what the long-term implications actually are. One of the most pressing of those is self-employment taxes. In addition to whatever it is decided that you owe by way of income tax, you'll owe an additional 15.3% on the first $160,200 of net profits no matter what.

This money is designed to cover Social Security and Medicare taxes - factors that are usually handled by a traditional employer. In a freelance situation, that burden falls on you. If you're not aware that you have to pay this amount, or if you're not able to accurately estimate what it might be given your income, it could end in a significantly larger tax bill than you had assumed you'd be facing.

Along the same lines, many new freelancers in particular are surprised to find out that they're supposed to pay taxes throughout the year - not just once like everyone else. Indeed, quarterly estimated tax payments are mandatory and if you don't handle this, you could be hit with penalties before you even have a chance to properly file.

If you get hit with a large tax bill at the end of the year because you hadn't been paying quarterly, you could always ask for a monthly payment plan with the IRS to settle your balance. Note, however, that this does not mean that your next round of estimated tax payments won't immediately come due. This is a situation where it is easy to fall behind on your taxes and, with penalties and interest, watch that "Past Due Balance" grow and grow. Even though things will be "fine" from a certain perspective so long as you keep up with your agreed-upon monthly payments, it could still be difficult to "get ahead" once again.

For many freelance employees, figuring out what deductions they're allowed to take given their job is not just a tax challenge - it's a general bookkeeping one as well. This will largely depend on what type of freelance work you're doing. If you're working for a company like Lyft or Uber, for example, you should be tracking the miles you drive while you're on the clock. You'll be able to deduct a portion of not only your gas but also your maintenance and insurance costs based on that information. But you can only do so if you've been tracking it accurately all along.

Typically, expenses fall into two distinct categories. "Ordinary" expenses are those that are common and that are traditionally accepted for your business. "Necessary" expenses, on the other hand, are those that are deemed "necessary" for your business.

The aforementioned business mileage while working for a ride-sharing company would be a common expense, for example. The same is true of any dues that you have to pay to even take the job, or subscriptions that are being paid out to organizations related to your business. Necessary expenses would be certain tools and other pieces of equipment that you cannot perform your job without.

Some of these challenges are the reason why, according to another recent study, 70% of people see freelancing as a viable career option when it exists alongside a traditional 9 to 5 job. Have a traditional employer handle at least some of the tax burden in a way that makes things easier overall. That doesn't mean you can get away with not thinking about bookkeeping and taxes at all, however, as the universal challenges outlined above go a long way towards proving.

If nothing else, all of this serves as an important reminder of why people need to enlist the help of an experienced financial professional to handle bookkeeping, tax, and related challenges. It's clear that the instinct to "do it all themselves" is a strong one within Generation Z. If it wasn't, they wouldn't be collectively so passionate about freelance work in the first place.

But this is one of those situations where it is extraordinarily easy to "get things wrong" and if you do, you could wind up in a financial situation that is difficult to recover from. Enlisting the help of a financial professional can help prevent these problems from happening early on, allowing Generation Z (and everyone else, for that matter) to enjoy all the benefits of freelancing with as few of the potential downsides as possible.